Fintech is no longer vertical; embedded finance models are gaining traction as financial services are delivered via products in sectors such e-commerce, agriculture, mobility, energy, health, and more.

There is increasing excitement around the growth of fintech companies across emerging markets, enabled by:

- talent availability;

- vast unmet demand for financial services;

- favourable regulations in certain markets;

- and improved mobile and internet infrastructure.

The ecosystem of support fintechs across emerging markets has grown tremendously in recent years as well, with many more accelerators, incubators and mentorship programs, as well as angel networks, in place to support early-stage entrepreneurs. As a result, the world has witnessed progress across emerging markets over the last decade.

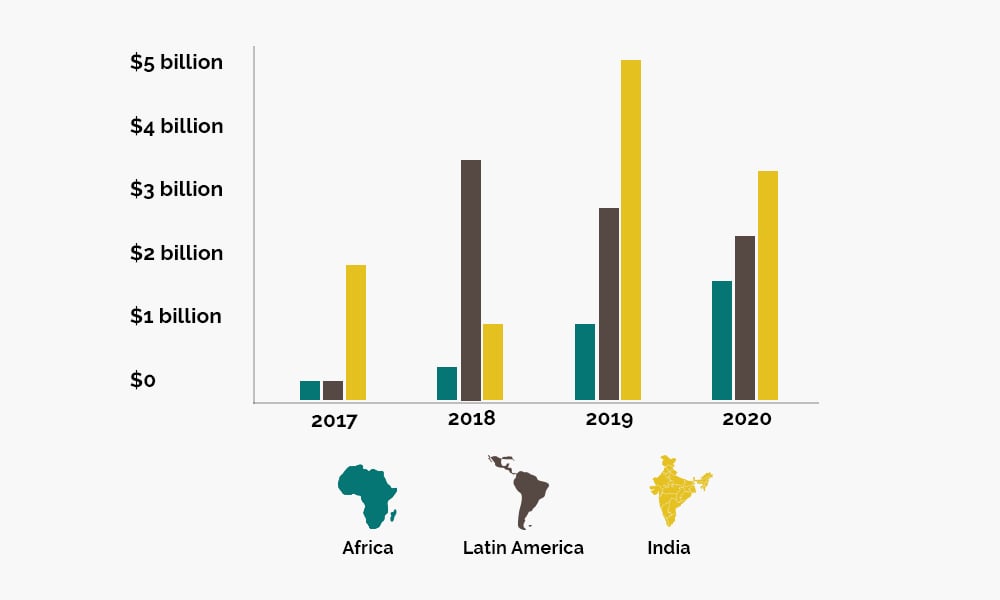

The fintech sector across emerging markets has boomed over the past five years. Since 2017, a growing number of both global and local VCs have invested an estimated $23 billion in fintech companies across Africa, Latin America and Asia. Fintech as a sector continues to receive the largest share of investment across emerging markets year-on-year, and this trend has accelerated post the COVID-19 pandemic.

Total fintech funding by region over last 5 years

Source – proshareng.com

In Africa, there were about 362 disclosed investment deals in the year 2020. These deals amounted to $1.2 billion in total and $2.4 billion including M&A deals. Of these totals, $1.35 billion went to fintech ($362 million excluding M&A).

The growth in funding flows into Africa has been enabled by:

· a growing population of 1.2 billion people;

· growing digitally savvy youth;

· rising smartphone ownership and mobile money adoption;

· reducing internet cost;

· and wider recognition of the opportunity to reach 350 million unbanked adults.

The 350 million unbanked adults account for 60% of the total population in Sub-Saharan Africa and around 17% of the unbanked population across the globe.

There has been an acceleration in digitization of consumer behavior and the demand for digital financial services post Covid-19 in Sub-Saharan Africa. For example, while the number of cashless payments was already rising, the pandemic has supercharged this trend, and startups have taken notice. This trend will likely persist throughout 2021 and beyond, and the world is likely to see greater uptake of digital-only banking services and wallets, especially if fintech companies continue to react and adapt to these changes.

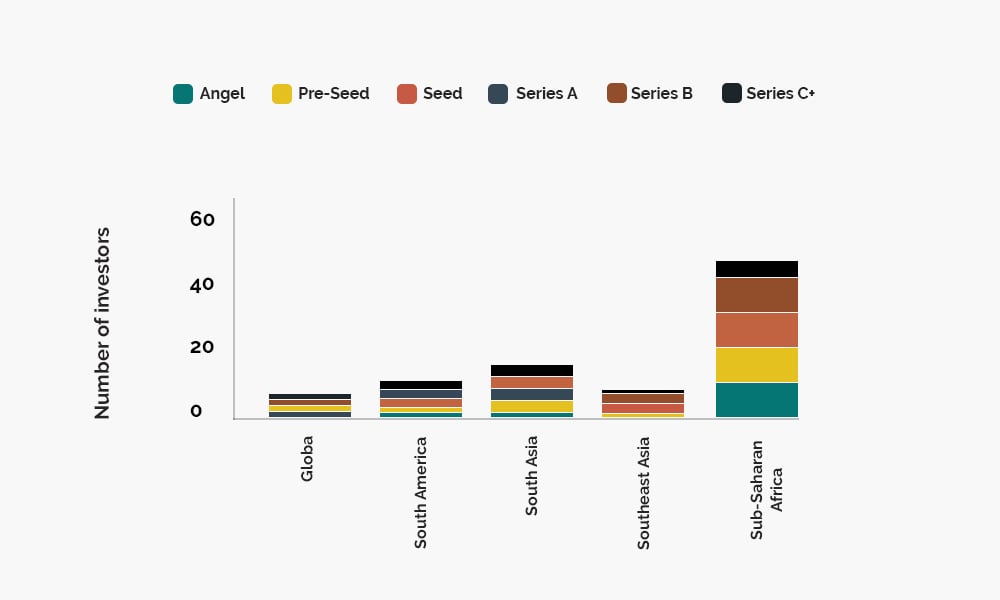

Investments in Sub-Saharan Africa

Source – proshareng.com

The numbers of pre-seed and seed deals in Sub-Saharan Africa is increasing, but the average size of these deals remains lower than that of other regions; seed rounds in Africa average around $1 million. Moreover, the African markets are beginning to see a few late-stage deals. Africa has witnessed fast-growing M&A activity, involving global brands such as Airtel Money, VISA, Network International, and Stripe, and African startups such as MFS Africa, Interswitch, and Paystack.

According to Reuters, Airtel Money (Airtel Africa’s fintech arm) has recently signed a $100 million investment partnership with Mastercard. This partnership will help expand Airtel Money’s mobile money business by adding new functionalities including linking up mobile money wallets with credit cards. The collaboration will also facilitate broader payment processing for cross-border transactions through the utilization of a payments gateway run by Mastercard.

Telecom operators’ mobile money units are making a foray into mobile remittances in many African economies. According to the World Bank remittance flows to sub Saharan Africa (excluding Nigeria) have increased by 2.3% in 2020. With Covid-19 restrictions, mobile money transfers have played a significant role as delivery channels, especially with platforms such as EcoCash in Zimbabwe, M-Pesa in Kenya, and others partnering with remittance companies for money to be transferred directly into mobile wallets.

Final Thoughts

There are a number of opportunities for investors and fintech startups to continue to develop innovative and inclusive financial services. Although fintechs are making strides towards greater financial inclusion, excluded segments (e.g., women, rural, poor, unbanked populations) remain a small proportion of fintech users as most companies remain focused on higher income and mainstream users. The COVID-19 pandemic has highlighted the structural inequalities more than ever. To address this gap, startups can lead the way in developing more accessible, affordable, and appropriate solutions for poorer people, vulnerable consumers and small businesses.

Comments